- Policy Rate Chart

- Housing Price Trends

- New Home Price Index

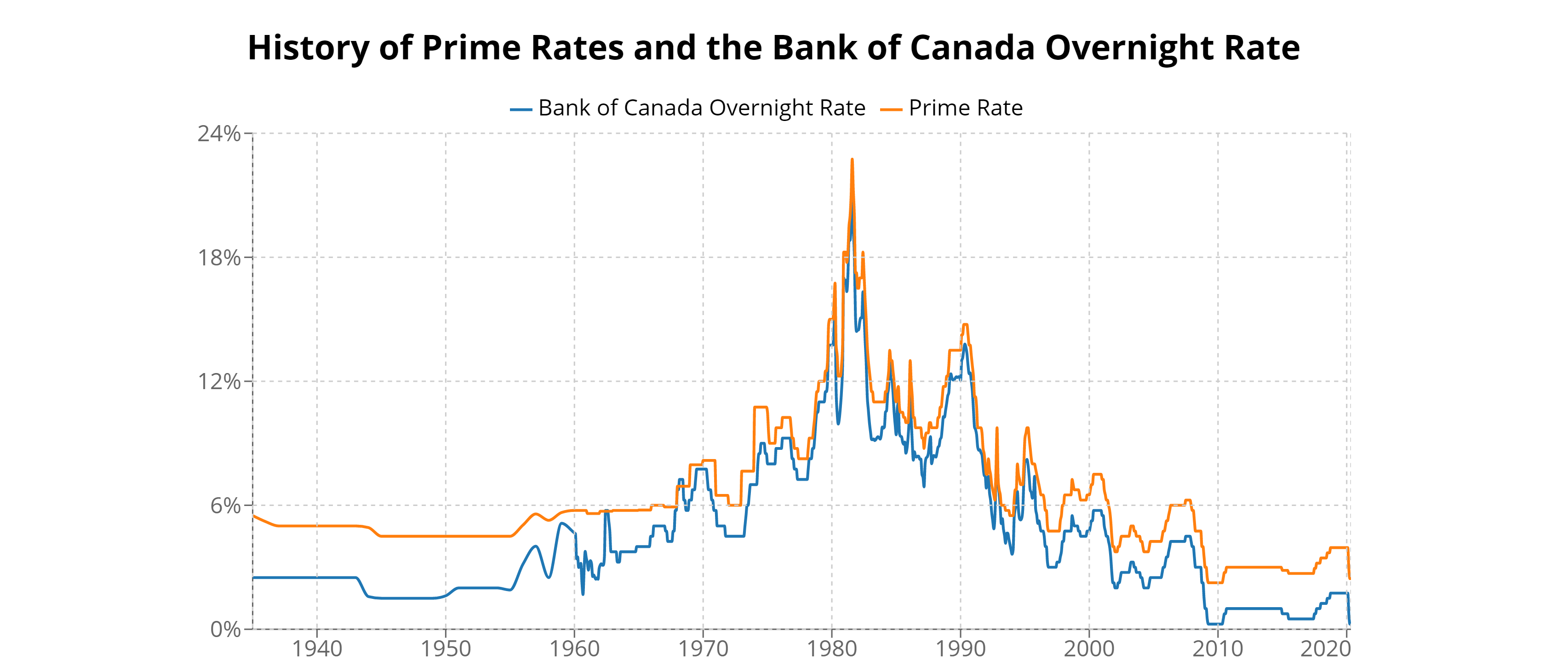

The chart above shows how the Bank of Canada has gradually shifted from its tightening stance toward easing, bringing the overnight rate down to 2.25% as of October 2025. After two years of elevated rates, this is a signal that the central bank sees growth risks outweighing inflation concerns.

Canadian home prices remain elevated, particularly in Ontario and B.C., though momentum has slowed since mid-2024. The Bank’s rate cut may provide some near-term relief to variable-rate borrowers and first-time buyers, but affordability challenges and supply shortages continue to shape the market.

The New Home Price Index reflects that some regions, especially in Ontario and the Prairies, have experienced mild price declines in new builds. Builders are cautious amid cost pressures and slower demand — but the lower rate may revive construction and investment confidence in 2026.

As seen above, mortgage rates closely follow the Bank’s policy trend. This easing cycle could signal a period of lower financing costs through mid-2026 — a potential turning point for the housing market.